ITR Forms Explained (AY 2026-27)

Which ITR Form Should You File for FY 2025-26 (AY 2026-27)?

CBDT notified all ITR forms on March 30, 2026. This year brings meaningful changes including expanded eligibility for ITR-1 and new disclosure requirements. Before you file, take five minutes to read this.

Every year, as the ITR filing season opens, one question comes up more than any other "Which form should I use?" It sounds like a formality. It is not.

Choosing the wrong ITR form is not merely a technical slip. The Income Tax Department can issue a defective return notice under Section 139(9) of the Income Tax Act, 1961, giving you only 15 days to rectify it. Miss that window and your return is treated as if it was never filed. Refund delays, loss carry-forward issues, and AIS mismatches can follow you well into the next assessment year.

For FY 2025-26 (AY 2026-27), the Central Board of Direct Taxes (CBDT) notified all ITR forms ITR-1 to ITR-7, along with ITR-U and ITR-V on March 30, 2026. Here is everything you need to know before selecting your form.

⚖️ Governing Law for AY 2026-27 ImportantThe new Income Tax Act, 2025 came into force on April 1, 2026. However, since AY 2026-27 covers income earned during FY 2025-26 (April 1, 2025 to March 31, 2026), these returns are still governed entirely by theIncome Tax Act, 1961. Familiar section references 80C, 80D, 24(b), 87A, 112A remain fully applicable for this filing season. The Act 2025 framework will apply only from AY 2027-28 onwards.

What's New in AY 2026-27 Key Changes at a Glance

Before diving into each form, here are the changes that directly affect which form you should pick this year:

1. ITR-1 and ITR-4 Now Cover Two House Properties

In previous years, ITR-1 and ITR-4 were limited to taxpayers with income from only one house property. From AY 2026-27, both forms now permit reporting of income from up to two house properties. A salaried individual with one self-occupied property and one rented or vacant property can now continue filing the simpler ITR-1, provided all other eligibility conditions are met. Previously, they would have had to shift to ITR-2.

2. LTCG up to ₹1.25 Lakh Now Reportable in ITR-1 and ITR-4

Taxpayers can now report long-term capital gains under Section 112A (from listed equity shares and equity-oriented mutual funds) in ITR-1 and ITR-4, provided: (a) the total LTCG does not exceed ₹1.25 lakh during the year, and (b) there are no brought-forward or carry-forward capital losses. Previously, any capital gains meant mandatory filing of ITR-2.

⚠️ Watch OutEven a single rupee of short-term capital gains, or LTCG exceeding ₹1.25 lakh, takes you out of ITR-1 and into ITR-2 or ITR-3. Check your AIS and broker statements carefully before assuming ITR-1 applies.

3. Dual Capital Gains Reporting Requirement Removed from ITR-2

In AY 2025-26, ITR-2 filers had to report capital gains separately those arising before July 23, 2024 and those on or after that date because of mid-year rate changes introduced by the Finance Act, 2024. Since no such mid-year rate change applies for FY 2025-26, this dual reporting requirement has been removed. Capital gains are now reported in a single schedule.

4. New Field for Unrealised Rent

A new mandatory field has been added in ITR-1, ITR-2, and ITR-4 to disclose the amount of rent that could not be realised from tenants, as per provisions under Section 23 read with Rule 4 of the Income Tax Rules, 1962.

5. Granular Deduction Disclosure Under 80C and 10(13A)

Deductions under Section 80C and HRA under Section 10(13A) must now be disclosed with greater specificity. On the e-filing portal, the exact clause or sub-section must be selected from a dropdown rather than entering a consolidated figure.

6. TDS Section Must Be Specified

A new field in the TDS schedule requires taxpayers to mention the specific TDS section under which tax was deducted helping the department reconcile TDS credit claims more accurately.

7. Aadhaar Enrolment ID No Longer Valid

The 28-digit Aadhaar Enrolment ID will no longer be accepted. Only a valid 12-digit Aadhaar number is permitted while filing returns for AY 2026-27.

8. Extended Due Date for ITR-3 and ITR-4 (Non-Audit)

The due date for non-audit cases filing ITR-3 and ITR-4 has been extended to August 31, 2026 (earlier it was July 31). The ITR-1 and ITR-2 due date remains July 31, 2026 for non-audit individuals and HUFs.

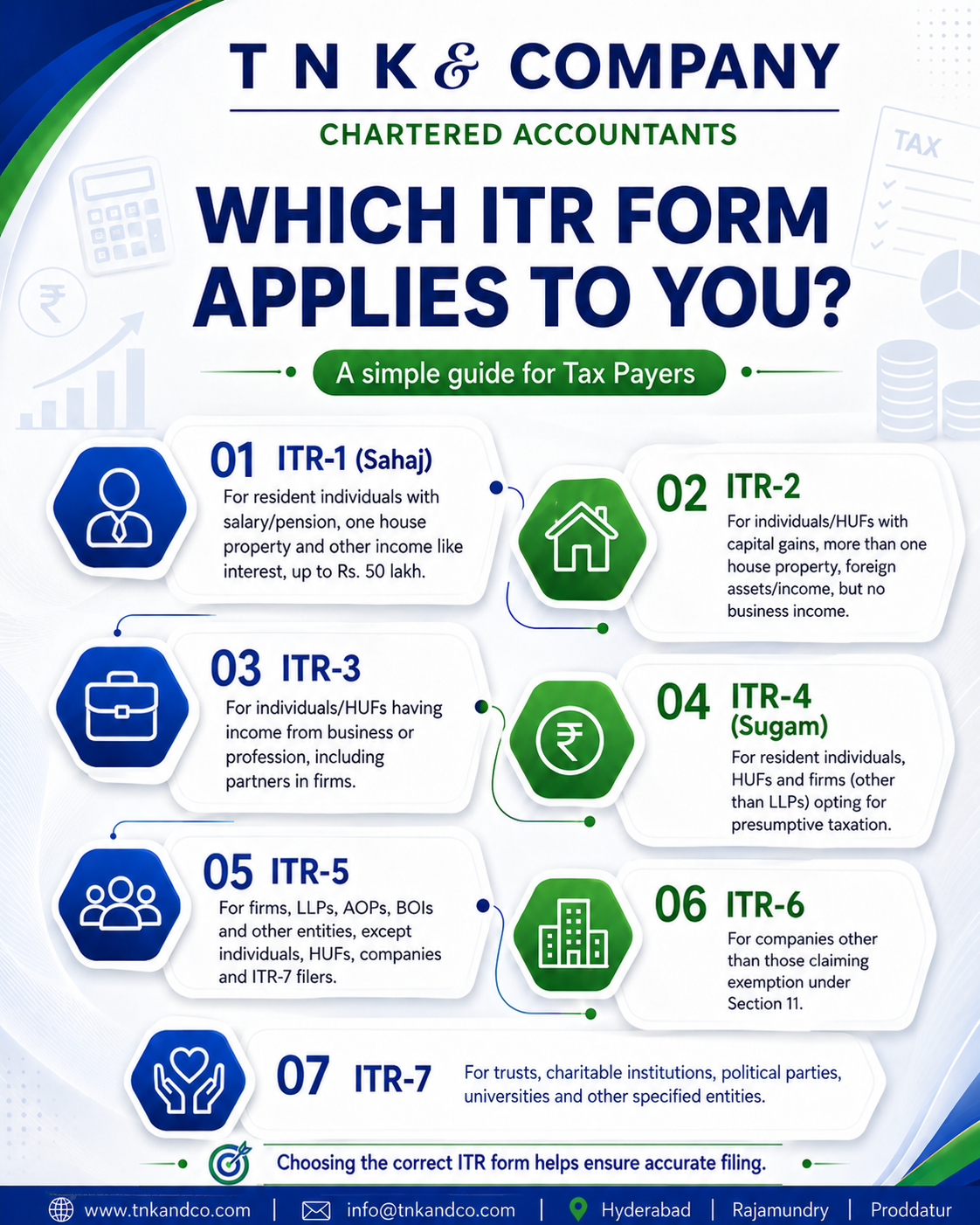

Which ITR Form Applies to You?

ITR-1 For the Salaried Resident Individual

Sahaj is exactly what its name suggests straightforward. It is designed for resident individuals whose income comes from predictable, limited sources.

You can file ITR-1 if:

- You are a resident individual (not NRI, not RNOR)

- Your total income does not exceed ₹50 lakh

- Income is from salary or pension, up to two house properties, other sources (interest, dividend, family pension), and agricultural income up to ₹5,000

- You have LTCG under Section 112A up to ₹1.25 lakh with no carried-forward capital losses

You cannot file ITR-1 if:

- You have business or professional income of any amount

- You have short-term capital gains or LTCG above ₹1.25 lakh

- You are a Director in any company

- You hold unlisted equity shares

- You have foreign assets, foreign income, or are an NRI/RNOR

- You have income from more than two house properties

- You have brought-forward or carry-forward losses under any head

ITR-2 For Capital Gains, NRI, and Complex Income

ITR-2 is for individuals and HUFs who do not carry on a business or profession, but whose financial life is more complex than what ITR-1 can accommodate.

File ITR-2 when you have:

- Capital gains of any kind from shares, mutual funds, property, or any other asset

- Foreign assets or foreign income (bank accounts, investments, employment abroad)

- NRI or RNOR residential status

- Income from more than two house properties

- Agricultural income exceeding ₹5,000

- Directorship in a company or investment in unlisted equity shares

- LTCG under Section 112A exceeding ₹1.25 lakh, or any short-term capital gains

If your income also includes business or professional income, ITR-2 will not suffice you would need ITR-3.

ITR-3 For Business Owners and Professionals

ITR-3 is the comprehensive form for individuals and HUFs with income from business or profession. It covers the full spectrum of income salary, capital gains, house property, other sources, and business/professional income, all in one return.

File ITR-3 if you are:

- A professional Chartered Accountant, doctor, advocate, architect, consultant, engineer

- A proprietor carrying on any business or trade

- An individual with income from F&O trading or intraday trading

- A partner in a firm receiving salary, bonus, commission, or interest from the firm

- A digital creator or freelancer earning professional income

- Any individual or HUF with business income that does not qualify for or opt for presumptive taxation

💡 Note for CAs in PracticeA Chartered Accountant in practice will generally need to file ITR-3, unless gross receipts are within the prescribed threshold and the CA opts for presumptive taxation under Section 44ADA in which case ITR-4 may apply.

ITR-4 For Eligible Taxpayers Under Presumptive Taxation

ITR-4 (Sugam) is designed for taxpayers who opt for the presumptive taxation scheme under Chapter XIV-C of the Income Tax Act, 1961. Under this scheme, income is computed at a prescribed percentage of turnover or gross receipts, removing the need for detailed books of accounts.

Applicable sections:

- Section 44AD eligible businesses (turnover up to ₹3 crore; or up to ₹10 crore if digital receipts threshold is satisfied)

- Section 44ADA specified professionals (gross receipts up to ₹75 lakh; or up to ₹1.5 crore if digital receipts threshold is satisfied)

- Section 44AE goods transport operators

Eligible to file ITR-4 if:

- Resident individual, HUF, or partnership firm (not LLP) with income up to ₹50 lakh

- Opting for presumptive taxation under the above sections

- May also have income from up to two house properties and LTCG u/s 112A up to ₹1.25 lakh

Cannot file ITR-4 if you:

- Are an LLP (file ITR-5 instead)

- Are an NRI or RNOR

- Have foreign assets or foreign income

- Are a Director in a company or hold unlisted equity shares

- Have total income exceeding ₹50 lakh

⚠️ New Disclosure for AY 2026-27ITR-4 filers this year must disclose details of investments in the financial particulars section, along with mandatory disclosure of bank balance as at March 31, 2026. Ensure your financial records are updated before filing.

ITR-5 For Firms, LLPs, AOPs, and Similar Entities

ITR-5 is applicable to entities that are not individuals, HUFs, companies, or persons required to file ITR-7. This includes partnership firms, Limited Liability Partnerships (LLPs), Association of Persons (AOPs), Body of Individuals (BOIs), co-operative societies, local authorities, and certain business trusts.

An LLP is always required to file ITR-5 and cannot opt for ITR-4, regardless of income levels or business nature.

ITR-6 For Companies

ITR-6 is applicable to all companies private limited or public limited registered under the Companies Act, 2013 or under any other law, except companies claiming exemption under Section 11 of the Income Tax Act, 1961 (income from property held for charitable or religious purposes). Such exempt entities generally need to verify ITR-7 applicability.

ITR-7 For Trusts, Institutions, and Political Parties

ITR-7 is prescribed for persons required to file returns under Sections 139(4A) to 139(4F) of the Income Tax Act, 1961. This covers:

- Charitable and religious trusts registered under Sections 12A or 12AB

- Political parties under Section 139(4B)

- Scientific research associations, universities, colleges, and hospitals

- Other specified institutions and investment funds where specifically required

Quick Reference Table

|

Form |

Popular Name |

Generally Applicable to |

|

ITR-1 |

Sahaj |

Resident individuals salary/pension, up to 2 house properties, other sources, LTCG u/s 112A up to ₹1.25 lakh; total income up to ₹50 lakh |

|

ITR-2 |

Individuals & HUFs without business income but with capital gains, foreign assets, NRI/RNOR status, multiple properties, company directorship |

|

|

ITR-3 |

Individuals & HUFs with business or professional income proprietors, CAs, doctors, traders, F&O income |

|

|

ITR-4 |

Sugam |

Eligible resident individuals, HUFs & firms (not LLPs) opting for presumptive taxation u/s 44AD, 44ADA or 44AE; income up to ₹50 lakh |

|

ITR-5 |

Partnership firms, LLPs, AOPs, BOIs, co-operative societies, local authorities |

|

|

ITR-6 |

Companies other than those claiming Section 11 exemption |

|

|

ITR-7 |

Charitable/religious trusts, political parties, universities, hospitals, specified institutions |

Due Dates for AY 2026-27

|

Category |

Applicable Form(s) |

Due Date |

|

Individuals & HUFs (non-audit) |

ITR-1, ITR-2 |

July 31, 2026 |

|

Individuals, HUFs, Firms non-audit |

ITR-3, ITR-4 |

August 31, 2026 |

|

Audit cases (all categories) |

All forms |

October 31, 2026 |

|

Transfer Pricing cases |

All forms |

November 30, 2026 |

|

Belated / Revised returns |

All forms |

March 31, 2027* |

*A late fee under Section 234F is applicable for belated returns. For revised returns filed after December 31, 2026, a fee under Section 234-I is payable.

Common Mistakes That Lead to Notices

These are the most frequent errors we see taxpayers make while selecting their ITR form:

- Filing ITR-1 despite having short-term capital gains or LTCG above ₹1.25 lakh

- Not shifting from ITR-1 to ITR-2 after taking up a directorship in any company

- Ignoring foreign assets or foreign bank accounts, which mandatorily require ITR-2 or ITR-3

- Selecting ITR-4 without verifying whether the conditions for presumptive taxation are actually satisfied

- Reporting F&O losses in ITR-1 or ITR-4 F&O income is business income and requires ITR-3

- Ignoring income appearing in the AIS that indicates a change in income profile

- Assuming residential status is the same as last year without re-checking

- Carrying forward the same form used last year without reviewing the current year's transactions

Documents to Keep Ready Before Filing

- PAN and 12-digit Aadhaar

- Form 16 from employer / Form 16A from deductors

- Form 26AS, Annual Information Statement (AIS), and Taxpayer Information Summary (TIS)

- Bank account statements and interest certificates

- Capital gains statements from broker and mutual fund house

- Home loan interest and principal certificate (for Section 24 and 80C claims)

- Rent receipts or rent agreement (for HRA claims under Section 10(13A))

- Investment proofs for deductions under Sections 80C, 80D, 80G, etc.

- Advance tax and self-assessment tax challans (Form 280)

- Books of accounts / financial statements (for ITR-3, ITR-5 filers)

- Foreign asset and foreign income details, if applicable

Before You File

The right ITR form is not determined by which form you used last year or which one is the simplest. It is determined by your actual income profile for FY 2025-26 your sources of income, residential status, capital transactions, directorship, foreign assets, and the legal structure you operate under.

A salaried individual with only salary and interest income may comfortably file ITR-1. The same person, upon making a capital gain on shares or taking up a directorship in a startup, moves to ITR-2. If they also have freelance income, it becomes ITR-3. The form follows the facts not the other way around.

If you are unsure which form applies to your situation, it is always better to consult a Chartered Accountant before filing than to deal with a defective return notice afterward.

Have Questions? We're Here to Help

Get expert advice from T N K & COMPANY. Reach out to discuss your requirements.